When Your Premium Stayed High After the Car Note Ended

You made the final payment on your 2016 sedan two years ago, completed the state-approved defensive driving course last spring, and your renewal notice arrived last month showing the same collision premium you carried when the bank required it. The mature-driver discount appeared as a line item, but your total annual cost dropped $140 while collision alone runs $480 per year. You drive 4,000 miles annually now that work commutes are gone, your vehicle's trade-in value sits around $6,200 according to the valuation tool your credit union provides, and you are paying full-coverage rates for protection that may no longer earn its cost.

This is the exact coverage-fit question lenders never let you ask and agents rarely surface once the loan obligation ends. Georgia law requires insurers to offer at least a 10% discount when you complete an approved defensive driving course, but that statutory floor applies to your base premium calculation before coverage selections multiply the total. The collision coverage protecting a paid-off vehicle of modest value operates under different math than the same coverage on a financed $35,000 purchase, and no renewal notice will tell you when the threshold tips.

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free QuoteGeorgia Statutory Discount Floor

10%

O.C.G.A. §33-9-42 requires insurers to offer at least a 10% discount to drivers 25 and older with clean records who complete a state-approved defensive driving course. The discount applies to your base premium calculation; carriers may exceed the floor but never state by how much without a filed quote.

O.C.G.A. §33-9-42

The Collision Coverage Question No Lender Lets You Answer

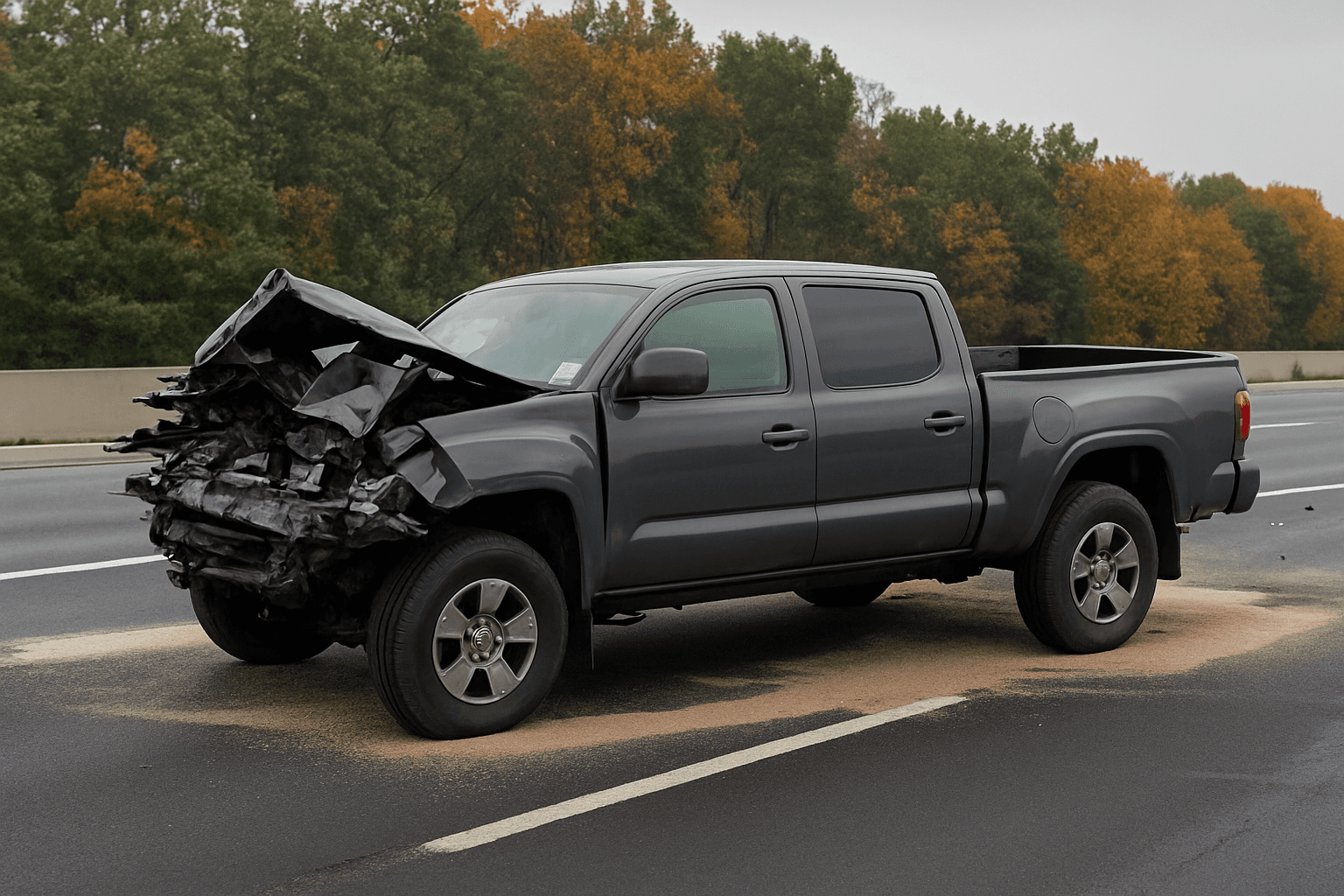

Collision coverage pays to repair or replace your vehicle when you cause an accident or hit an object, minus your deductible. When a lender holds the title, full coverage including collision is mandatory: the bank's asset requires protection until you own it outright. The day you make the final payment, that requirement vanishes, but your policy renews automatically at the same coverage level unless you intervene. Most retirees in Athens continue carrying collision on paid-off vehicles for months or years simply because no notice flags the structural shift.

The coverage-fit calculation turns on three numbers: your vehicle's current replacement value, your collision deductible, and your annual collision premium. If your car is worth $6,200, your deductible is $500, and collision costs $480 per year, you will pay $1,440 over three years to protect $5,700 of net value after the deductible. A single at-fault accident recovers that cost. Two claim-free years and you have paid most of the protected value in premiums alone. The math does not make collision irrational on a paid-off vehicle, but it makes the decision yours rather than the lender's, and the threshold sits lower than most retirees expect.

You are paying collision premiums to protect equity you already own outright, and no carrier will tell you when your three-year premium total approaches your vehicle's replacement value.

The Coverage Path That Fits Your Actual Risk

Liability coverage pays the other party's costs when you cause an accident: their vehicle repair, medical bills, lost wages, and legal fees if they sue. Georgia's statutory minimums are $25,000 per person for bodily injury, $50,000 per accident, and $25,000 for property damage, but retirees with retirement accounts, home equity, or other assets exposed in a lawsuit often carry $100,000/$300,000/$100,000 or higher. Collision protects your vehicle; liability protects your assets from the other driver's claim. One coverage defends what you drive, the other defends what you own, and the asset-protection role grows more critical as your retirement savings accumulate while your vehicle depreciates.

Comprehensive coverage pays for non-collision damage: theft, vandalism, weather events, falling objects, animal strikes, and glass breakage. In Athens, summer hail and deer strikes are common enough that many retirees keep comprehensive even after dropping collision. Comprehensive premiums run lower than collision because the risk profile differs, deductibles apply the same way, and the coverage remains worthwhile on older vehicles where collision math tips negative. A $6,200 sedan hit by hail or stolen from a grocery parking lot triggers a comprehensive claim; the same vehicle totaled in an at-fault accident you caused triggers collision. The former happens to you, the latter because of you, and insurers price that distinction clearly.

Related Articles

What Changes at Your Next Renewal and What Stays

Dropping collision mid-term requires contacting your carrier or agent directly; coverage changes do not process automatically when a loan payoff posts. Most insurers allow mid-term changes with a prorated refund for the unused collision premium, but some apply administrative fees or restrict changes to renewal dates depending on their filed rules with the Georgia Department of Insurance. Confirm the effective date of the change, the refund amount if applicable, and whether your comprehensive deductible can differ from the collision deductible you previously carried. Some retirees lower their comprehensive deductible to $250 when dropping collision, trading a modest premium increase for lower out-of-pocket cost on glass or hail claims.

Your liability limits, uninsured motorist coverage, and medical payments coverage remain in place regardless of collision decisions. These coverages protect you and others in accidents you do not cause or in scenarios where the at-fault driver lacks insurance. Georgia does not require uninsured motorist coverage, but UM pays your costs when an uninsured driver hits you and collision would not apply because you did not cause the accident. Retirees dropping collision sometimes add UM or increase UM limits to offset the protection gap, though UM pays only when another driver is at fault and identifiable. Hit-and-run scenarios and single-vehicle accidents you cause remain unprotected once collision is gone.

The mature-driver discount applies to your revised premium calculation the same way it applied before the coverage change. Completing a state-approved defensive driving course every three years keeps the discount active; the certificate expiration date controls eligibility, and most carriers remove the discount automatically at the first renewal after expiration unless you submit a new certificate. Some retirees set a calendar reminder six months before expiration to re-enroll, ensuring the new certificate posts before the old one lapses. The 10% statutory floor means your discount will never fall below that threshold as long as your course completion is current, but carriers set their own filed amounts and some exceed the minimum without advertising it.

Georgia Bodily Injury Minimum Per Person

$25,000

Georgia requires $25,000 per person, $50,000 per accident for bodily injury, and $25,000 for property damage as the liability floor. Retirees with assets exceeding these limits face exposure in at-fault accidents where the other party's costs surpass your coverage, and raising liability limits costs far less than collision on a paid-off vehicle.

Georgia Department of Driver Services

How Athens Carriers Handle Low-Mileage and Course-Discount Combinations

Twenty-five carriers write auto insurance in Georgia, spanning preferred, standard, and non-standard tiers. Geico, Progressive, State Farm, and Nationwide offer online quoting and operate in the standard tier with explicit mature-driver and low-mileage programs. Geico's low-mileage discount applies when you certify annual mileage below 7,500 miles and verify it through their app or odometer photos at renewal; the mature-driver course discount stacks separately and requires submitting your certificate through their online portal. Progressive offers Snapshot, a usage-based program tracking mileage and driving patterns through a plug-in device or app, and their mature-driver discount applies automatically when your age and course certificate meet eligibility.

State Farm processes course certificates through local agents rather than online upload, and their Drive Safe & Save program monitors mileage via smartphone app with discounts applying at each renewal based on verified data. Retirees in Athens report smoother certificate processing through agents who specialize in senior drivers and handle renewals proactively, though online-quote carriers like Geico and Progressive offer faster initial quotes and transparent discount visibility during the shopping process. Some carriers apply the low-mileage discount at quote time based on your stated annual mileage; others require enrollment in a monitoring program and apply the discount only after the first renewal verification cycle completes.

Comparing carriers means requesting quotes at identical liability limits and coverage structures. A $100,000/$300,000/$100,000 liability quote with comprehensive, no collision, $250 deductible, and both mature-driver and low-mileage discounts applied gives you a fair baseline. Some carriers show discount line items separately; others embed them in the base premium calculation and never surface the pre-discount figure. Ask each carrier how their mature-driver discount applies, whether course completion requires annual re-verification or works on a three-year cycle matching certificate expiration, and whether their low-mileage program involves device installation, app check-ins, or annual odometer reporting.

When Full Coverage Still Earns Its Cost on a Paid-Off Vehicle

Vehicle value alone does not resolve the collision question. A retiree whose paid-off vehicle is their only transportation and who lacks liquid savings to replace it after an at-fault total loss may find collision worth keeping even when the annual premium approaches 10% of the car's value. The coverage buys certainty: one at-fault accident and the claim pays replacement value minus deductible regardless of how many claim-free years preceded it. Retirees with $15,000 in accessible savings and a second household vehicle often make a different call than those whose emergency fund sits at $3,000 and the car represents their sole mobility.

Collision makes clearest sense when your vehicle's value significantly exceeds three times your annual collision premium and you drive enough miles that at-fault accident probability remains non-trivial. A paid-off 2020 vehicle worth $18,000 with $600 annual collision premium and 8,000 miles driven yearly sits in different territory than a 2014 vehicle worth $6,200 with $480 annual premium and 3,500 miles. The former protects meaningful equity at reasonable cost; the latter protects diminishing value at a cost that compounds faster than the car depreciates. No universal threshold applies, but when your collision premium exceeds 8% of your net vehicle value annually, the math starts tipping.

Compare Liability-Plus-Comprehensive Against Your Current Full-Coverage Cost

Request quotes from at least three carriers writing in Georgia with your actual liability limits, comprehensive coverage with your preferred deductible, no collision, and both mature-driver and low-mileage discounts applied. State your annual mileage honestly; odometer verification at renewal will surface discrepancies and some carriers rescind low-mileage discounts retroactively when reported mileage does not match verified totals. Confirm that each quote includes the mature-driver discount and ask whether submitting your course certificate is required at quote time or at policy bind.

Compare the liability-plus-comprehensive quote against your current full-coverage renewal premium. The difference is what you are paying annually to protect your vehicle's net value after deductible in at-fault scenarios you cause. Multiply that difference by three and compare it to your vehicle's current replacement value: if three years of collision premiums approach or exceed what your car is worth, the coverage has likely crossed the threshold where dropping it makes financial sense for your household. If three years of premiums represent less than half your vehicle's value and you drive enough that at-fault risk remains present, keeping collision remains defensible.