The Last Payment Brings a Question, Not an Answer

You made the final car payment and your agent called to congratulate you. Then they asked whether you still want collision and comprehensive. You expected clarity after decades of ownership, but now you face a choice lenders used to make for you.

The standard advice points to vehicle value: drop full coverage when the car is worth less than ten times your annual premium. For a retiree on fixed income, that threshold misses the real question. How long would it take to replace this car from savings if it were stolen or totaled tomorrow, and what would you drive in the meantime?

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free QuoteGeorgia Liability Floor Per Person

$25,000

Georgia requires $25,000 bodily injury per person, $50,000 per accident, and $25,000 property damage. These minimums protect the other driver, not your own vehicle. Without collision and comprehensive, your paid-off car has no coverage for theft, weather damage, or accident repairs.

O.C.G.A. Title 33, Chapter 34

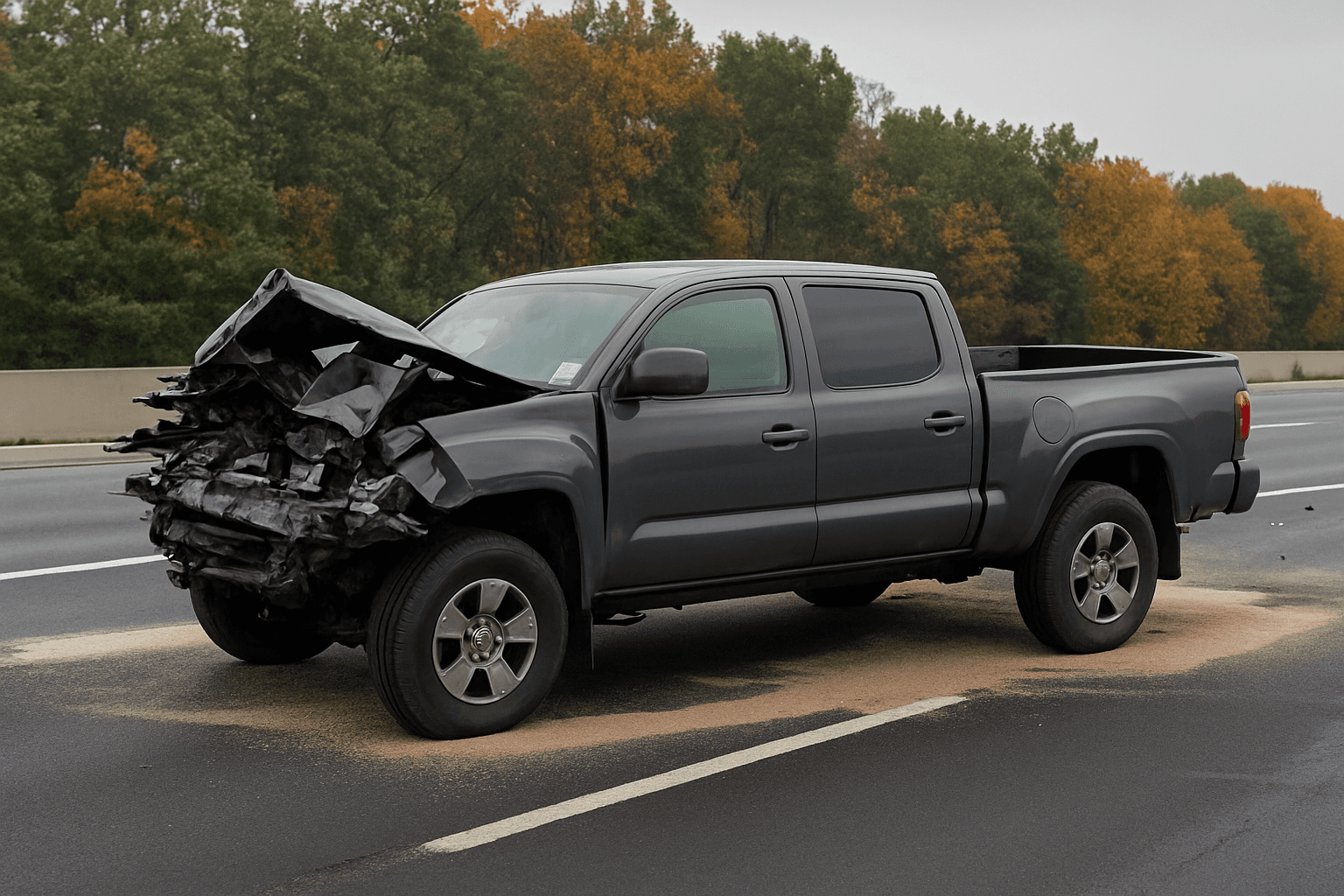

What You Actually Give Up When You Drop Full Coverage

Collision covers damage to your car when you hit another vehicle or object, regardless of fault. Comprehensive covers theft, vandalism, hail, flood, fire, and animal strikes. Liability-only means you pay out of pocket for all of those, even when you did nothing wrong.

Georgia's fault system means the other driver's liability coverage should pay for your car if they caused the accident. But liability-only leaves you exposed in three common scenarios: hit-and-run with no identified driver, the at-fault driver carries only Georgia's $25,000 property-damage minimum and your vehicle exceeds that figure, or weather and theft events where no other driver exists to file against.

Retirees often drive vehicles worth less than $10,000, which sounds modest until a flood totals the car or a deer strike requires $4,500 in repairs. The question is not whether the car is valuable in the abstract. The question is whether you can replace it from savings faster than monthly premiums would rebuild that amount.

The blocker is informational: you cannot resolve the full-coverage question until you know how long rebuilding a replacement fund from premium savings would actually take.

How to Calculate Your Replacement Timeline

Call your current carrier or use their online portal to request a quote for liability-only on your existing policy. Subtract that figure from your current premium. The difference is your monthly savings if you drop collision and comprehensive. Multiply by twelve to find your annual savings, then divide your car's private-party value by that annual figure. The result is how many years of savings it would take to rebuild a replacement fund equal to your current vehicle's worth.

If that timeline exceeds the number of years you expect to drive this car, dropping full coverage means you will self-insure a vehicle you plan to replace before the fund grows large enough. If the timeline is shorter than your expected ownership period, you reach breakeven before the car ages out. Georgia retirees who drive fewer than 5,000 miles annually often find the timeline stretches five years or longer because low-mileage premiums keep the monthly savings modest.

Related Articles

Georgia-Specific Factors That Bend the Standard Advice

Metro Atlanta's vehicle-theft rate sits above the national average for cities its size, with older sedans and trucks among the most frequently stolen models. Comprehensive covers theft regardless of your car's book value. If you park in a high-theft ZIP code or your model appears on Georgia's annual theft report, comprehensive may justify its cost even when collision does not.

Georgia's tornado season and summer hail create comprehensive claims unrelated to driving behavior. A paid-off 2015 sedan parked in a driveway can incur $6,000 in hail damage in fifteen minutes. Liability coverage pays nothing. Your savings absorb the full loss unless comprehensive remains in force.

Medical Payments coverage and Personal Injury Protection interact with Medicare in ways most retirees misunderstand. Medicare covers hospital and doctor bills after an accident, but it does not cover your car. Some retirees drop full coverage assuming Medicare protects them, but Medicare's scope stops at medical expense. Your vehicle repair or replacement still requires collision or comprehensive, or comes from savings.

If you keep comprehensive but drop collision, verify with your carrier that they allow split coverage. Most do, but a few require both or neither. Splitting makes sense when theft and weather worry you more than accident damage, particularly for drivers whose annual mileage dropped below 3,000 and whose neighborhood sees frequent catalytic-converter theft.

Carriers Writing Georgia Auto

25

Twenty-five carriers write personal auto insurance in Georgia, including high-risk specialists and preferred-tier insurers. Mature-driver discounts and low-mileage programs vary widely. Comparing full-coverage pricing across three to five carriers often uncovers a rate $40 to $70 per month lower than your current premium, changing the replacement-timeline math entirely.

Georgia Department of Insurance carrier filings

When Keeping Full Coverage Makes Sense After the Last Payment

Full coverage justifies its cost when your replacement timeline exceeds your expected ownership period and the premium difference is modest enough that dropping coverage saves less than $500 annually. It also makes sense when your savings cannot absorb a total-loss event without forcing you to delay other retirement expenses or rely on family help.

Georgia retirees who completed a state-approved defensive driving course receive at least a ten-percent discount on their premium under O.C.G.A. § 33-9-42. That floor applies to collision and comprehensive, not only liability. Verify that your carrier applied it. If the discount was never filed or lapsed when your certificate expired, reinstating it can lower your full-coverage premium enough to shift the replacement-timeline calculation in favor of keeping it.

Compare Carriers Before You Drop Coverage

Most retirees compare full-coverage cost only against liability-only cost on their current policy. That frames the question as keep-versus-drop. A better frame compares full-coverage cost across carriers that write Georgia auto and offer mature-driver discounts. The lowest full-coverage quote often sits below your current liability-only premium, eliminating the tradeoff entirely.

Request quotes from at least three carriers writing in your county. Name your annual mileage, your defensive-driving course completion if applicable, and your vehicle's paid-off status. Some carriers reduce comprehensive premiums for garaged vehicles or apply additional discounts for drivers over 65 with no claims in the prior three years. These are not advertised; you learn them at quote time.

What to Do Right Now

Call your current carrier or log into your account portal. Request a liability-only quote and confirm whether your mature-driver discount is active. Calculate your replacement timeline using the method above. If the timeline is short and your savings can absorb a total loss, schedule the coverage change effective your next renewal date. If the timeline is long or your savings cannot cover replacement, request full-coverage quotes from two additional Georgia carriers before you make any change.