Updated June 2026

What Is Collision Coverage Insurance?

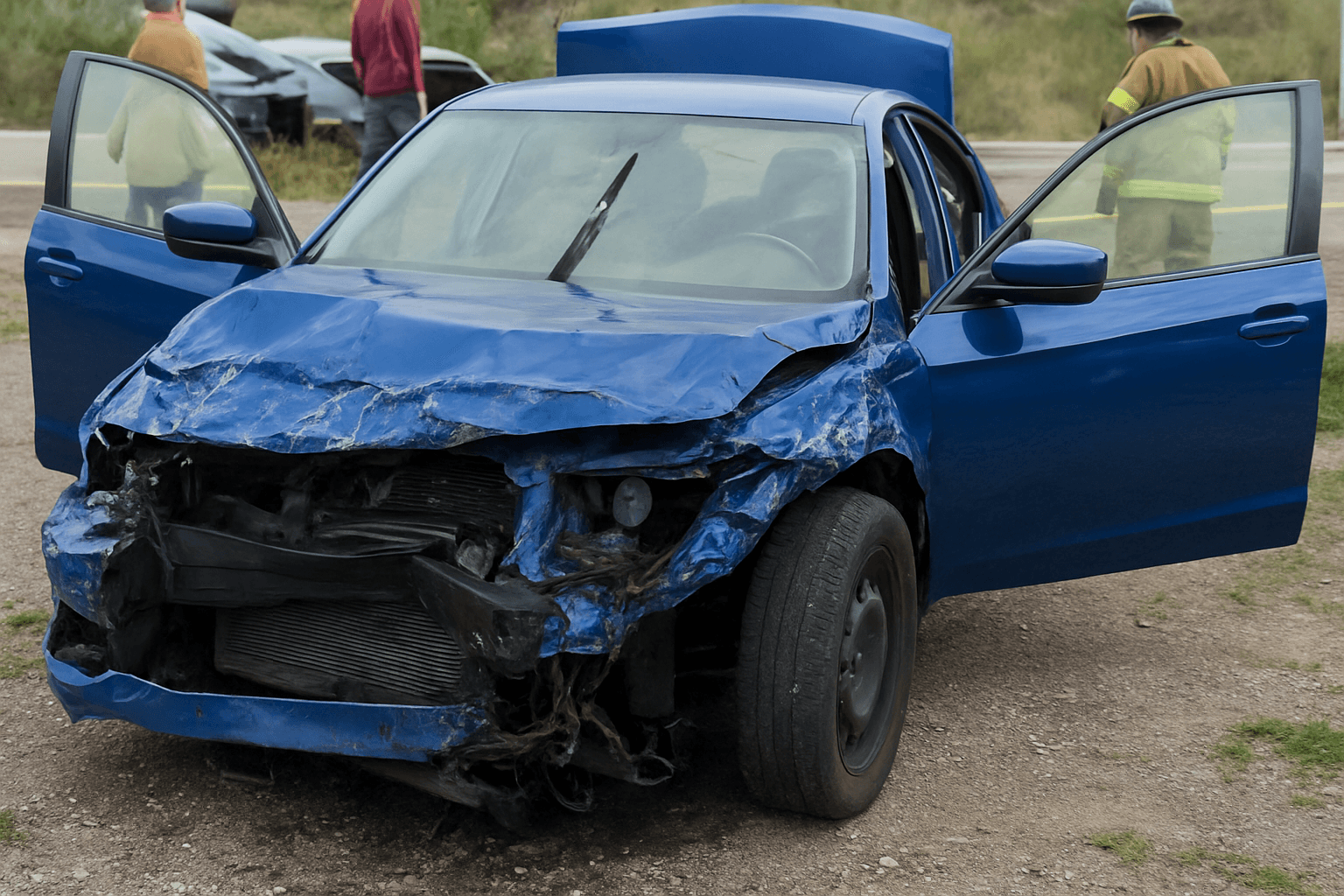

Collision coverage repairs or replaces your vehicle after a crash with another car, a stationary object like a guardrail or pole, or a rollover. It pays your claim whether you caused the accident or the other driver did. The insurer pays the actual cash value of your vehicle minus your chosen deductible, up to policy limits. If repair costs exceed the vehicle's pre-accident value, the insurer declares it a total loss and pays you that value.

- You rear-end a car at a stoplight, causing $4,200 in damage to your vehicle and $6,800 to theirs. Your collision coverage pays the $4,200 minus your $500 deductible, so you receive $3,700 for your repairs. Your liability coverage handles the other driver's $6,800 vehicle damage and any medical bills. Without collision coverage, you pay the full $4,200 out of pocket.

- Someone hits your parked car overnight and leaves without a note. Repairs cost $3,100. Your collision coverage pays $3,100 minus your $1,000 deductible, so you receive $2,100. The at-fault driver is unknown, so their liability coverage can't be pursued. Uninsured motorist property damage coverage might apply in some states, but Georgia doesn't mandate it and most policies here don't include it.

- You swerve to avoid debris on I-75, lose control, and roll your SUV into a ditch. The vehicle is totaled. Its actual cash value before the accident was $8,400. Your collision coverage pays $8,400 minus your $500 deductible, so you receive $7,900. No other driver is involved, so liability coverage doesn't apply. Without collision coverage, you absorb the full $8,400 loss and replace the vehicle from savings.

Who Needs Collision Coverage Insurance?

Retirees still making payments on a vehicle must carry collision coverage per lender contract. If you own your car outright and it's worth more than ten times your annual collision premium — for example, a $15,000 vehicle with $1,200 annual collision cost — the coverage makes sense because you can't replace the car from one year's premium savings. Drivers with clean records and limited savings who can't absorb a $6,000–$12,000 loss without financial strain should keep it.

Divide your vehicle's current actual cash value by your annual collision premium including deductible. If the result is under 8, consider dropping collision and setting aside the premium in a vehicle replacement fund. If it's over 12, keep the coverage. Between 8 and 12, your decision hinges on savings cushion and risk tolerance — carriers won't tell you this ratio because they profit when you overpay for coverage on depreciated assets.

How Much Does Collision Coverage Insurance Cost?

Collision coverage typically adds $35–$95 per month to a Georgia retiree's premium, or $420–$1,140 annually, depending on vehicle value, deductible choice, driving record, and ZIP code.

- Vehicle replacement cost — a $12,000 sedan costs less to insure for collision than a $38,000 SUV because the maximum payout is lower.

- Deductible amount — choosing a $1,000 deductible instead of $250 can reduce collision premium by 25–40 percent.

- Claim history — a collision claim in the past three years raises your premium even if you weren't at fault, because it signals statistical risk to the insurer.

- Garaging ZIP code — urban areas with higher accident rates and repair costs in metro Atlanta carry steeper collision premiums than rural counties.

- Vehicle age and depreciation — collision coverage on a 12-year-old car with $4,000 actual cash value may cost $600 annually, returning less than seven times premium in a total-loss scenario.

- Bundled discounts — pairing collision and comprehensive coverage often unlocks a multi-coverage discount that lowers the combined cost by 10–15 percent.