Updated June 2026

What Is Liability Insurance Insurance?

Liability insurance is the only coverage Georgia law requires you to carry. It splits into two parts: bodily injury liability, which pays medical bills, lost wages, and legal costs when you injure someone in an accident, and property damage liability, which pays to repair or replace the other driver's vehicle or damaged property. Your insurer defends you in court and pays settlements or judgments up to your policy limits, but once those limits are exhausted, you pay the rest out of pocket.

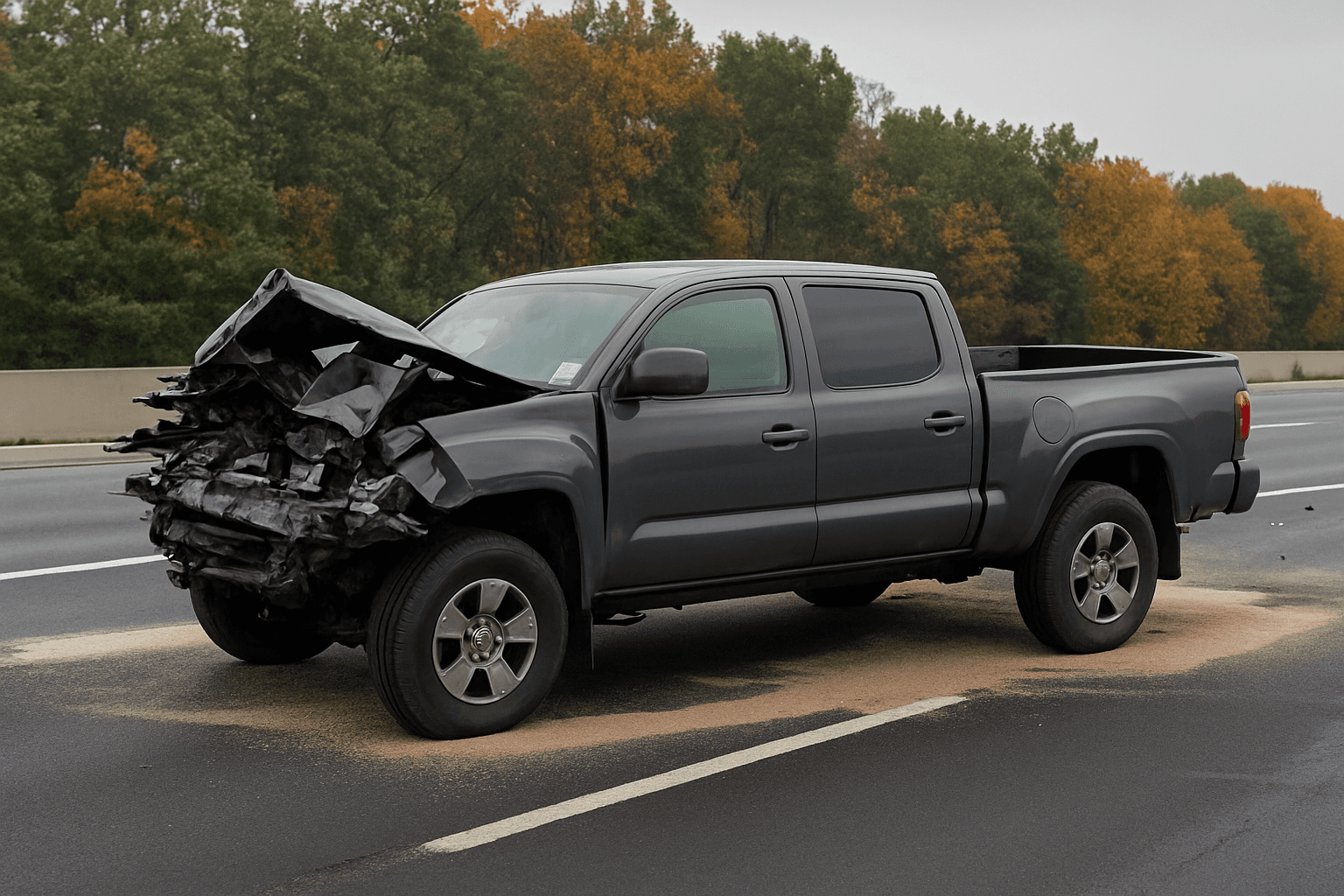

- You misjudge stopping distance in Atlanta traffic and rear-end the car ahead. The other driver has $18,000 in medical bills and $7,200 in vehicle damage. Your 25/50/25 policy pays the full $25,200 because it falls within your limits. Your own bumper damage costs $3,400 to fix — liability pays zero toward that, and you cover it yourself or file a collision claim if you carry that coverage.

- You cause a three-car pileup on I-285. Two people require hospitalization; their combined medical bills reach $110,000. Your $50,000 bodily injury limit pays out in full, but you're personally liable for the remaining $60,000 unless the injured parties settle for less or you declare bankruptcy. Retirees on fixed income face asset seizure risk when liability limits fall short — your paid-off home, savings, and retirement accounts are all reachable in a judgment.

- You sideswipe a contractor's truck carrying $22,000 worth of equipment. The truck repairs cost $8,500, and the damaged equipment totals $18,000 — a combined $26,500. Your $25,000 property damage limit pays out in full, leaving you liable for the remaining $1,500. Many retirees discover too late that state minimums were set decades ago and no longer cover the cost of modern vehicles or the cargo they carry.

Who Needs Liability Insurance Insurance?

Liability insurance is non-negotiable — Georgia law requires it to register a vehicle, and driving without proof risks license suspension, vehicle impoundment, and a $200 reinstatement fee under O.C.G.A. § 40-6-10. Retirees with assets to protect — a paid-off home, retirement accounts, or savings above $50,000 — should carry liability limits well above the state minimum, because a single serious accident can trigger a judgment that reaches those assets. If you still drive regularly or share the road during peak hours, higher limits are the cheapest protection you can buy against financial catastrophe.

Start by identifying what you'd lose in a lawsuit — equity in your home, retirement account balances, and cash savings are all reachable by judgment creditors in Georgia. If that total exceeds $50,000, carry liability limits of at least 100/300/100 and consider umbrella coverage above that. If you drive fewer than 5,000 miles per year and only in low-traffic conditions, the actuarial risk is lower, but your legal obligation and financial exposure remain the same — the decision is whether to protect assets or accept judgment risk, not whether to carry coverage.

How Much Does Liability Insurance Insurance Cost?

Liability-only policies in Georgia typically cost $45–$85 per month for drivers with clean records, or $540–$1,020 annually, depending on your county, driving history, and the limits you select above the state minimum.

- Liability limits you select — upgrading from 25/50/25 to 100/300/100 often adds $15–$30 per month but closes the gap between state minimums and real accident costs.

- Your zip code — metro Atlanta counties show higher liability premiums than rural Georgia due to accident frequency and average claim severity.

- Driving record — a single at-fault accident in the past three years can raise liability premiums 20–40 percent, even if no claim was filed.

- Credit-based insurance score — Georgia allows insurers to use credit history in pricing, and liability rates vary significantly between score tiers.

- Annual mileage — retirees driving under 7,500 miles per year often qualify for low-mileage discounts that reduce liability costs 5–15 percent.

- Mature driver course completion — Georgia insurers must offer a discount to drivers who complete an approved defensive driving course, though the percentage varies by carrier and is set in individual rate filings.