The Paid-Off Car Decision

You opened your renewal notice and the premium hasn't changed even though you paid off the car loan two years ago, dropped your daily commute, and completed the state-approved defensive driving course. The collision and comprehensive line items add up to more per year than the car's private-sale value would bring, and you're questioning whether you're insuring against a loss you could absorb.

This article walks the coverage-fit decision for retirees in Savannah with paid-off vehicles. Georgia requires insurers to offer at least a 10% discount to drivers who complete an approved defensive driving course, but the discount doesn't automatically make full coverage the right call. The real question turns on what you'd lose if the car were totaled tomorrow versus what you're paying annually to protect against that scenario, adjusted for Savannah's theft and weather risk.

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free QuoteGeorgia Mature-Driver Discount Floor

10%

Georgia law requires insurers to offer at least a 10% discount to drivers 25 and older with clean records who complete a state-approved defensive driving course. Carriers may exceed this floor, but the statute sets the minimum you can claim.

O.C.G.A. §33-9-42

What Full Coverage Actually Protects

Full coverage means liability plus collision plus comprehensive. Liability is mandatory: Georgia requires $25,000 per person and $50,000 per accident for bodily injury, and $25,000 for property damage. That minimum never changes regardless of whether your car is paid off.

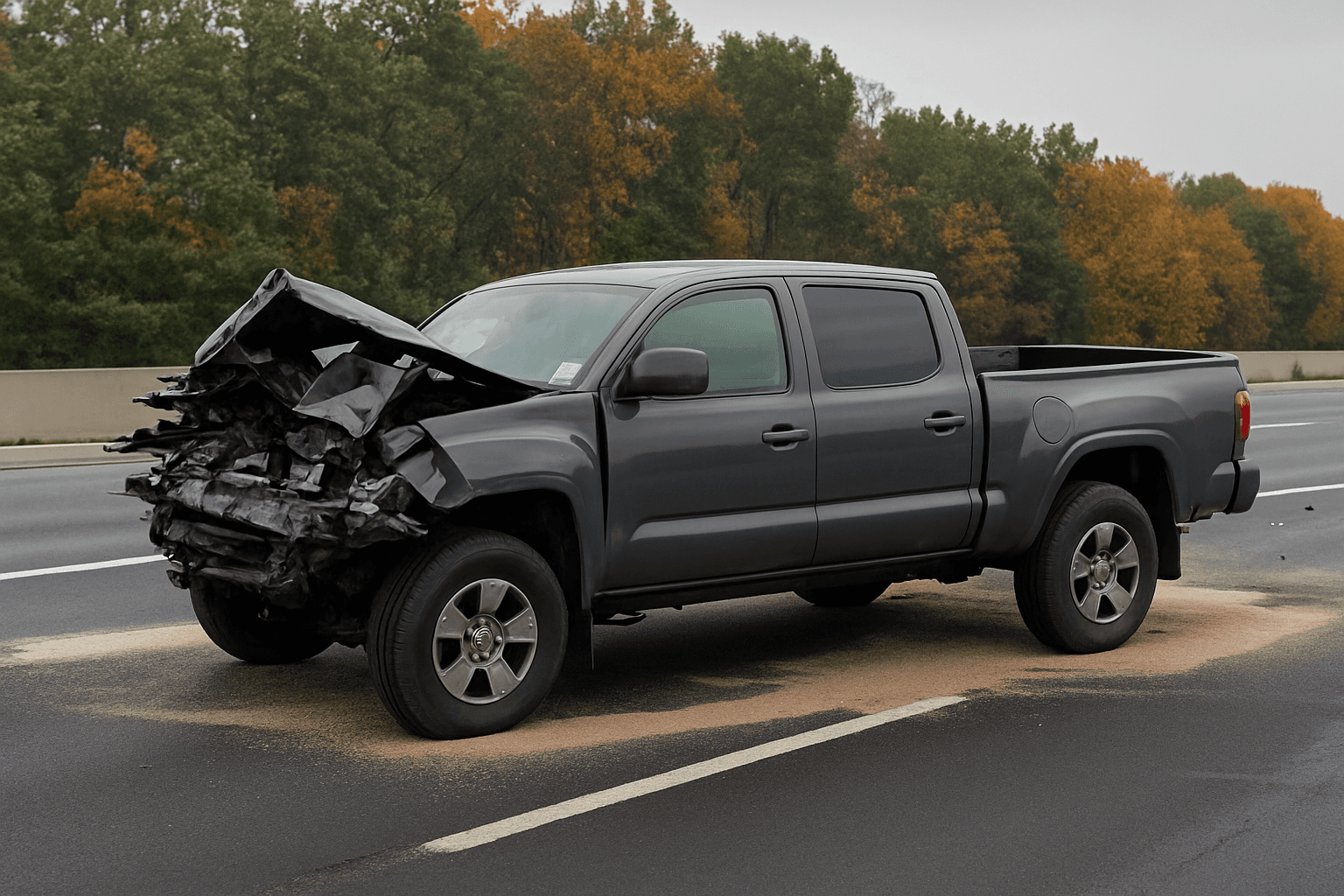

Collision pays to repair or replace your car after an accident you caused or a hit-and-run. Comprehensive pays for theft, vandalism, weather damage, and animal strikes. Both have deductibles, and both pay only up to the car's actual cash value at the time of loss. If your 2017 sedan is worth $8,000 in today's market and you carry a $1,000 deductible, collision and comprehensive protect a net $7,000 exposure.

Once the loan is satisfied, no lender forces you to carry collision or comprehensive. The decision becomes purely economic: does the annual premium cost less than the financial impact of replacing the car out of pocket if it's totaled or stolen? For retirees on fixed income, that calculation includes whether you have liquid savings to replace the vehicle without disrupting other financial commitments.

The coverage decision isn't whether the car is paid off. It's whether you can replace it tomorrow without financial strain if it's stolen or totaled tonight.

Savannah's Theft and Weather Context

Chatham County, where Savannah sits, reports higher property crime rates than Georgia's rural counties. Comprehensive claims for theft and vandalism occur more frequently in urban Savannah ZIP codes than in surrounding areas. If you park on the street overnight or in an unsecured lot, that exposure is real. Conversely, if your car stays in a locked garage in a low-crime neighborhood, the theft risk drops materially.

Hurricane season brings flooding and wind damage. Savannah's elevation and proximity to the coast make comprehensive coverage relevant during tropical weather events. A paid-off sedan damaged by storm surge or falling debris still costs thousands to repair or replace, and comprehensive is the only coverage that pays for weather losses not caused by collision.

Related Articles

The Arithmetic for Low-Mileage Retirees

Pull your current policy declarations page and find the annual cost of collision and comprehensive combined. Divide that figure by the car's current private-sale value to calculate your premium-to-value ratio. If you're paying $900 per year to insure a car worth $7,000, you're spending 12.9% of the vehicle's value annually on physical-damage coverage.

Compare that ratio against your financial position. If you have $7,000 in liquid savings earmarked for vehicle replacement and losing the car wouldn't disrupt your budget, dropping collision and comprehensive saves the premium every year. If replacing the car would require liquidating other assets, taking a loan, or disrupting retirement income, the premium buys peace of mind and budget predictability.

Consider repair-cost sensitivity. A $2,500 repair bill on a paid-off car you plan to drive another five years may be manageable with savings. A total loss requiring immediate replacement of a vehicle you depend on for medical appointments, errands, and family visits is a larger financial event. The coverage decision turns on which scenario creates more financial stress for your household.

Georgia Bodily Injury Minimum Per Person

$25,000

Georgia's liability floor is $25,000 per person, $50,000 per accident for bodily injury, and $25,000 for property damage. Retirees with retirement accounts or home equity face exposure above these minimums in an at-fault accident. Liability limits are independent of whether you carry collision or comprehensive.

O.C.G.A. Title 33, Chapter 34

What Happens When You Drop Coverage

Dropping collision and comprehensive mid-term triggers a premium refund for the unused portion of your policy period. Contact your carrier or agent, request the change in writing, and confirm the new premium and effective date. Most carriers process the change within days and issue a refund check or apply the credit to your next renewal.

Once the change is effective, your policy pays only for liability losses and any optional coverages you kept, such as medical payments or uninsured motorist. If your car is damaged in an accident you caused, stolen, or totaled by weather, you receive nothing from your insurer. You pay out of pocket to repair or replace the vehicle.

You can reinstate collision and comprehensive at any time by contacting your carrier, but the premium recalculates based on the car's current value and your current rating factors. If your driving record changed or the carrier repriced your risk class, the reinstated premium may differ from what you paid originally.

Liability Limits Matter More After You Drop Physical Damage

Retirees often carry retirement accounts, home equity, and other assets an at-fault accident judgment can reach. Georgia's $25,000 per person bodily injury minimum covers only modest medical bills. A serious injury easily exceeds that floor, and the injured party can pursue your assets beyond the policy limit.

If you drop collision and comprehensive to save premium, redirect part of those savings toward higher liability limits. Moving from $25,000/$50,000 to $100,000/$300,000 bodily injury coverage costs less than continuing full physical-damage coverage on a paid-off car, and it protects the assets you've accumulated over decades. Liability insurance is the coverage that shields everything you own beyond the car itself.

Medical payments coverage coordinates with Medicare for retirees injured in an accident. Medicare is primary, but med pay covers deductibles, copays, and passenger injuries without requiring you to file against your own liability policy. It's inexpensive and relevant regardless of whether you carry collision or comprehensive.

Compare Carriers That Serve Savannah Retirees Well

Georgia law requires insurers writing in the state to offer the mature-driver discount, but carriers differ in how they rate low-mileage drivers and handle paid-off vehicles. State Farm, GEICO, Progressive, Allstate, and Nationwide all write in Georgia and offer mature-driver and low-mileage programs. Ask each carrier whether completing the defensive driving course qualifies you for the discount, whether they offer a low-mileage or usage-based program, and what your premium would be with liability-only versus full coverage on your current vehicle.

Get quotes from at least three carriers. Provide your VIN, current mileage, garaging address in Savannah, and whether you completed the approved course. Compare not just the premium but the coverage structure: some carriers bundle uninsured motorist coverage at no additional cost, others charge separately. Some offer accident forgiveness after a clean period; others do not.

Request declarations pages in writing so you can compare coverages side by side. The lowest premium means nothing if the liability limits are inadequate or the carrier excludes coverages you need. Make the decision based on total cost for the coverage structure that fits your risk, not the headline number alone.